All Categories

Featured

Table of Contents

Insurance coverage business will not pay a minor. Rather, consider leaving the money to an estate or trust. For even more thorough information on life insurance get a copy of the NAIC Life Insurance Policy Buyers Overview.

The IRS puts a restriction on how much cash can go into life insurance costs for the plan and just how promptly such costs can be paid in order for the plan to retain every one of its tax obligation benefits. If certain limitations are gone beyond, a MEC results. MEC insurance policy holders may undergo tax obligations on distributions on an income-first basis, that is, to the degree there is gain in their policies, in addition to fines on any type of taxable quantity if they are not age 59 1/2 or older.

Please note that superior finances build up rate of interest. Revenue tax-free therapy additionally presumes the lending will at some point be pleased from revenue tax-free fatality advantage proceeds. Car loans and withdrawals lower the policy's money value and survivor benefit, might trigger certain plan advantages or riders to become unavailable and may boost the opportunity the plan may lapse.

A customer might certify for the life insurance, yet not the cyclist. A variable universal life insurance coverage contract is an agreement with the main function of providing a fatality advantage.

How do I compare Flexible Premiums plans?

These profiles are very closely managed in order to please stated investment objectives. There are fees and costs associated with variable life insurance contracts, consisting of mortality and risk fees, a front-end lots, administrative costs, financial investment management charges, abandonment costs and charges for optional bikers. Equitable Financial and its affiliates do not give lawful or tax suggestions.

And that's wonderful, since that's precisely what the death advantage is for.

What are the advantages of whole life insurance policy? One of the most enticing advantages of buying an entire life insurance coverage policy is this: As long as you pay your premiums, your fatality benefit will certainly never run out.

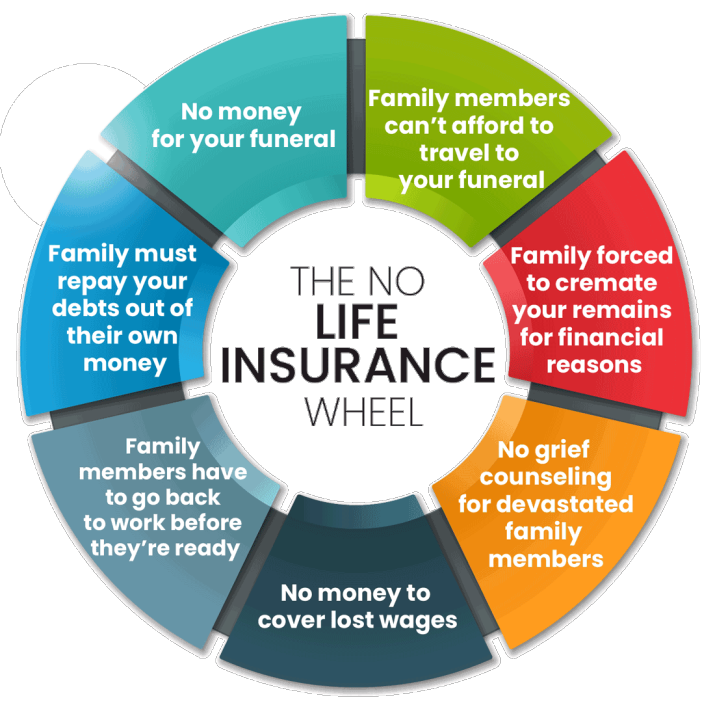

Believe you don't need life insurance if you don't have kids? You might intend to assume once again. It might appear like an unnecessary expense. But there are several advantages to living insurance, also if you're not supporting a family. Below are 5 reasons you must acquire life insurance policy.

What is the most popular Riders plan in 2024?

Funeral expenditures, interment expenses and medical expenses can accumulate (Term life insurance). The last point you desire is for your liked ones to carry this extra burden. Irreversible life insurance is readily available in different quantities, so you can select a survivor benefit that meets your demands. Alright, this just uses if you have youngsters.

Identify whether term or permanent life insurance policy is best for you. After that, obtain a quote of how much protection you may require, and exactly how much it might set you back. Locate the correct amount for your budget plan and comfort. Locate your amount. As your individual circumstances adjustment (i.e., marriage, birth of a kid or task promotion), so will your life insurance requires.

Generally, there are two sorts of life insurance policy prepares - either term or irreversible plans or some combination of both. Life insurers use various types of term strategies and standard life policies in addition to "interest delicate" products which have become much more widespread considering that the 1980's.

Term insurance gives defense for a specified duration of time. This duration might be as brief as one year or offer insurance coverage for a particular variety of years such as 5, 10, two decades or to a defined age such as 80 or sometimes as much as the oldest age in the life insurance policy mortality.

What is the best Guaranteed Benefits option?

Presently term insurance coverage prices are very affordable and among the cheapest historically experienced. It must be noted that it is a commonly held belief that term insurance coverage is the least expensive pure life insurance policy protection available. One needs to assess the plan terms meticulously to determine which term life choices appropriate to fulfill your certain situations.

With each brand-new term the costs is increased. The right to renew the policy without evidence of insurability is an essential advantage to you. Otherwise, the danger you take is that your health and wellness may weaken and you may be incapable to get a policy at the same rates and even in any way, leaving you and your recipients without protection.

You need to exercise this alternative during the conversion duration. The length of the conversion period will differ depending on the type of term plan purchased. If you transform within the proposed period, you are not required to offer any type of details regarding your health. The premium price you pay on conversion is typically based upon your "existing obtained age", which is your age on the conversion date.

Under a degree term plan the face quantity of the policy stays the exact same for the entire duration. With decreasing term the face quantity minimizes over the duration. The premium stays the very same each year. Typically such policies are sold as home mortgage defense with the amount of insurance coverage decreasing as the equilibrium of the mortgage reduces.

How do I apply for Term Life Insurance?

Generally, insurers have not had the right to transform premiums after the plan is sold. Considering that such policies might proceed for years, insurers must use conventional death, rate of interest and expense rate estimates in the premium computation. Flexible costs insurance, nonetheless, allows insurance companies to use insurance policy at lower "existing" costs based upon much less conventional assumptions with the right to change these costs in the future.

While term insurance is created to give defense for a defined amount of time, irreversible insurance coverage is developed to supply insurance coverage for your whole life time. To keep the costs price degree, the premium at the more youthful ages goes beyond the actual expense of security. This extra premium constructs a book (money worth) which helps pay for the policy in later years as the price of protection rises above the premium.

The insurance coverage firm invests the excess premium bucks This kind of plan, which is often called cash worth life insurance coverage, produces a cost savings component. Cash values are essential to a permanent life insurance coverage policy.

{kind=link}

Latest Posts

About Burial Insurance

Instant Whole Life Insurance Quotes Online

Funeral Planning Insurance